What is the Difference?

Credit card processing has become increasingly expensive for merchants, especially small businesses who have tighter budgets and may not bring in as much revenue as their larger competitors. By accepting credit cards, businesses face the financial burden of interchange fees, otherwise recognized as swipe fees. On average, swipe fees range from 1-4% and over time, can significantly turn profits into a loss for smaller businesses. As a result, many small businesses are looking for solutions to keep accepting cards, but avoid the monthly interchange fees. An answer to this dilemma was solved in recently formulated cash discount programs, which were federally authorized in all 50 states in 2011. However, there has been some confusion as to what a cash discount program is and how it varies from a surcharge. The following "Cash Discount Program" will discuss what the main differences are between a surcharge and a cash discount program, how to implement a legal and successful cash discount program, and what merchants should consider when evaluating cash discount providers.

What is a Surcharge?

A surcharge1 is a charge or fee that is added towards the price of a good or service and is usually added towards an existing tax. 40 states in the US allow surcharge fees to customers who pay with credit card. The remaining states that prohibit surcharges are California, Colorado, Connecticut, Florida, Kansas, Maine, Massachusetts, New York, Oklahoma, and Texas. Surcharges, however, cannot be assessed on debit cards.

1. http://www.nfib.com/content/legal-compliance/money/credit-card-surcharges-and-cash-only-discountswhat-you-need-to-know/

They are added simply for the privilege of using a credit card. Typically, surcharges are based on a specific percentage of the total price of goods or services before taxes are assessed.

What is a Cash Discount Program?

A cash discount occurs when a merchant decreases the price for cash purchases and offers merchants an alternative to credit card processing. Cash discount programs are not credit card surcharges because they do not levy a fee that is added to a credit card transaction.

There has been much confusion around cash discount programs in the past, as people tend to associate them with surcharge programs. The final verdict on cash discount programs can be found in the Durbin Amendment2 (part of the 2010 Dodd-Frank law), which states that businesses are permitted to offer a discount to customers as an incentive and to encourage customers to pay by alternative methods other than a credit/debit cards. Such alternative methods include checks or cash in order to receive a discount, which is applied at the time of sale.

A cash discount works by applying a small customer service fee on all customer transactions. This fee is removed if the customer pays with cash or in-store gift card. True cash discount technology will automatically determine the service fee or discount amounts depending on the payment type. Legal cash discount programs must present a clear receipt detailing the service fee or cash discount amount. Service fees are collected by the technology provider who then pays off the credit card charges on behalf of the merchant, essentially removing the need for any back-end accounting or complex statements. The merchant will usually see their credit card fees dramatically reduced with only a small technology fee to pay at the end of the month.

While state law may vary for surcharge programs, there has yet to be seen any direct language prohibiting a merchant implementing a cash discount program as long as consumers are notified prior to purchase.

Implementing a Legal and Successful Cash Discount Program

To implement a truly successful cash discount program, a merchant must overcome the

confusion and questions consumers and employees have surrounding a cash discount program.

At a minimum, a merchant is required to provide at least one point of notification prior to sale that there is a service fee applied to all sales and a discount given if a cash payment is made. Multiple points of notification are recommended -such as at the door, register of the store and throughout the establishment if needed. Additionally, the reference to the program should be made verbally at point of sale. It is important the correct language is used, such as “Would you like to save (X amount) today by paying in cash, or use your card?” This language clearly indicates the service charge applies to all transactions. It is also recommended the merchant has quick reference information handy to give to the customer if they have any additional questions.

Unlike surcharge programs, cash discount programs are seen in a better light, and fare better with the end-consumers. There has been a misconception that a cash discount program would prohibit sales if a customer does not carry cash.

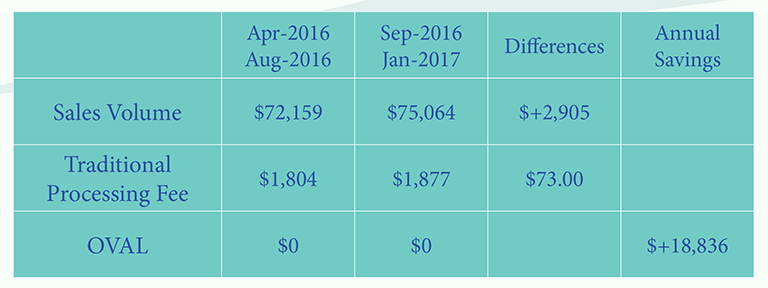

We’ve researched this with multiple merchants using Oval Payments and found it to be unbiased fear. In all cases, the credit card volume has remained consistent or even increased month over month, with reports from merchants that their customers disregard the convenience fee in 99.2% of transactions.

Things to Consider when Evaluating Cash Discount Programs

1. Legality – Not all cash discount programs are built the same. Make sure the provider you choose has good standing with the BBB and can provide clear evidence they adhere to all state and federal laws in their processes. In addition, ask to see a sample receipt. In order to adhere to federal standards, the cash discount program must show the service fee or discount amount clearly to the customer.

2. Equipment -Make sure the provider technology and equipment accepts all card types as well as mobile wallets and EMV chip cards. Cash discount technology does not work on all equipment brands. In fact, Oval Payments is the only provider of automated cash discount POS technology that follows federal compliance laws.

3. Hidden Costs -Some providers will require charge setup fees or hidden costs. In most cases, you can demand these be waived. Cash discount programs are simple in concept and a good provider will be completely transparent in their pricing and not charge unnecessary fees.

4. Fee Options -Good providers offer two service fee pricing options-either by an average ticket size (flat fee) or a percentage of the sale amount. Businesses with a big ticket discrepancy need the percentage model, while businesses with consistent average ticket size work well with a flat fee.

5. Support – For a successful rollout, merchants will need the cash discount supporting materials such as in-store signage, training guides and videos, quick reference handouts as well as a hotline to answer customer questions. A good provider will offer all of these things free of charge, in addition to being on-hand to troubleshoot equipment, answer billing questions, or assist with additional

training.